Monday, January 08, 2007

By Dian Hymer

Inman News

David Lereah, chief economist for the National Association of Realtors, recently said that the home sale market has started to stabilize and could even turn around by spring 2007. Other economists are less optimistic.

Ken Rosen, a noted real estate forecaster, predicts that it will take about three years for the San Francisco Bay Area housing market to turn around. Leslie Appleton Young, chief economist for the California Association of Realtors, thinks it will take 18 months for the California market to recover. But, in a recent survey conducted by WSJ.com, the Wall Street Journal's Web site, economists by a margin of 2 to 1 predicted that the worst was over for the housing market.

The opinions about the direction of home prices are equally diverse. Rosen sees home prices dropping by about 8 percent in the San Francisco Bay Area and 11 percent in Miami over the next few years. NAR predicts increases in home prices next year. Some think we've already hit bottom; others think we haven't hit bottom yet.

After this cycle is over, we'll be able to look back and pick the point at which excess inventory disappeared and home buyers were back in force. Until then it's anyone's guess as to exactly what the housing market will look like over the next few years.

Diverse opinions about the housing market are not unusual. For the last several years, many economists predicted interest rates in the 7 percent range for 30-year fixed-rate mortgages. But, that didn't materialize. In fact, lower rates fueled a hot market in which home prices rose at historic rates in many areas. This was at a time when most economists were sure that home prices had peaked.

Even though most housing experts would not recommend buying at the top of a market cycle, last years' home buyers bought with reckless abandon, confident that home prices could go nowhere but up. Now that conditions are generally better for home buyers, many are waiting on the sidelines for a clear sign that the market has bottomed out.

Most people feel more comfortable buying when there is a lot of home-buying activity. However, savvy real estate investors take a different approach. They buy when the market is soft and sell when the market is hot.

However, home buying and selling decisions are rarely based simply on whether it's the best time to buy or sell. This is because the "investor" is buying a property that will also function as a home.

Few home sellers who are happy in their current home sell just because the market is strong. On the other hand, no matter how content you are in your home, if your job moves elsewhere, you could find yourself having to sell in a soft market. Lifestyle factors impact home buying and selling decisions.

HOUSE HUNTING TIP: If you have the luxury of picking the time to buy or sell a home, you should first carefully analyze the housing market in your local area. It can be misleading to rely on a forecast that deals with the national housing market, or even a smaller regional market like the San Francisco Bay Area.

There are pockets of strength where demand is high and inventory low even in the midst of markets that are otherwise stagnant or declining. And, some markets like Utah and Washington state aren't declining at all.

THE CLOSING: When you have a grip on local market conditions, you'll be better able to decide if it makes sense to move now or to wait. But, keep in mind that waiting could cost you more if you're a buyer and yield you less if you're a seller, depending on how long you wait.

Dian Hymer is author of "House Hunting, The Take-Along Workbook for Home Buyers" and "Starting Out, The Complete Home Buyer's Guide," Chronicle Books.

__________________________________________________________________

Mortgage Originations Projected to Drop Through 2008

Fewer mortgages will be written in 2007 because of higher interest rates and a slowing housing market, predicts the Mortgage Bankers Association.

MBA Chief Economist Douglas G. Duncan told the Associated Press that markets are normalizing after historically low interest rates spurred record numbers of home owners to buy and refinance.

The Washington, D.C.-based trade group says it expects the total value of new mortgages and refinanced mortgages to drop 5 percent this year to $2.39 trillion from $2.51 trillion in 2006. The association projected a further drop of 4 percent to $2.29 trillion in 2008 as fewer home owners refinance their mortgage.

Mortgage originations had already declined 17 percent in 2006 from more than $3 trillion in 2005, a near-record year.

Source: The Associated Press, Eileen Alt Powell (01/09/07)

__________________________________________________________________

What to Know Before Buying a Fixer-Upper

A home in need of repair can be a good deal, especially if buyers are able to do some of the repairs themselves.

Here are three major things to think about when considering a home in need of lots of improvements:

Location, location location. Is the lot well located with good topography? Will the improvements you propose make it worth as much as — not a lot more — than other homes in the neighborhood?

How much? Calculate what the home would sell for if it were in great shape. Subtract the cost of repairs, then take off another 10 to 15 percent for unexpected problems. If you can’t get the property for that, then it's probably a bad deal.

Prepare for the mess. Get ready for renovations to take longer than expected. Know that your life will be disrupted if you can’t afford to live somewhere else while the work is being completed.

Source: Charlotte Observer, Kathy Haight (01/08/07)

__________________________________________________________________

30-Year Mortgage Rates Hold, Others Mixed

The financial markets during the first week of the year were still trying to determine how much the economy is likely to slowdown, according to experts. For the second consecutive week, Freddie Mac reported 30-year fixed loans averaged 6.18 percent.

However, other rates remained mixed. Interest on 15-year, fixed mortgages rose slightly to 5.94 percent, rates on five-year adjustable-rate mortgages moved up to 6.02 percent, and one-year ARMs slipped to 5.42 percent.

"Currently, the market is waiting for a clearer signal on the direction in which the economy is headed," says Frank Nothaft, Freddie Mac chief economist. Rates on 30-year loans declined over much of the second half of 2006 as the housing market continued to falter.

Source: St. Paul Pioneer Press, Martin Crutsinger (01/05/07)

© Copyright 2006 Information Inc.

___________________________________________________________________________

5 Tips for Selling a House in Foul Weather

Selling a home during the cold-weather months can be a challenge. Here are some tips for handling a sale in the dark winter months:

Don’t wait for spring. Point out to sellers that postponing can be the wrong choice when it means they must continue to pay the mortgage, insurance, and utility bills.

Get rid of the holiday decorations. “Holiday decor says to buyers that you aren’t prepared to move out so they can move in. It clutters and detracts from the home,” says Mark Nash, a real estate professional and author of the forthcoming book, Real Estate A-Z for Buying & Selling a Home.

Clean and light. Render the place dust-free and if necessary paint the walls with a light color. Linen tones are often the best.

Be creative. Nash, who sells homes in Chicago, had success last year selling an ordinary house quickly after he displayed poster-size photos of the home’s garden in full bloom near the windows.

Be realistic. No amount of creative marketing can overcome an overly steep price tag.

Source: Universal Press Syndicate, Ellen James Martin (01/04/07)

___________________________________________________________________________

Borrowers eye benefits of FHA home loans

Product offers lower rates, better choices than subprime sector

Monday, January 08, 2007

By Jack Guttentag

Inman News

"What type of borrower finds it advantageous to take an FHA loan?"

The answer to this question is a little different today than in 2000 when I first addressed it because FHA's market niche is smaller. This reflects developments in the conventional sector that have not been matched by FHA, including the growth in popularity of loans with no down payment, interest-only monthly payments, and option ARMs. Reflecting these developments, FHA's market share fell from about 15 percent in 2000 to about 5 percent in 2006.

The FHA Market Niche in 2006. An FHA borrower:

Has blemished credit acceptable to FHA, but not strong enough for prime pricing in the conventional market.

Doesn't need a loan larger than the FHA maximum, which varies by county. (In 2006, it ranged from $200,160 to $362,790 in the highest-cost counties.)

Can put 3 percent down in cash.

Doesn't want an interest-only mortgage or an option ARM.

Credit Requirements: At risk of oversimplifying, credit standards in the conventional market range from A+ to D-, and within that range, FHA would be about B- or C+.

FHA credit requirements overlap the higher levels of subprime requirements. A good illustration is the underwriting rules applicable to a prior foreclosure. With exceptions, FHA won't accept a loan applicant who has had a foreclosure within the prior three years. Subprime lenders may have a three-year rule for their best credit grade, but the period scales down by degrees and might be only one year for the lowest grade.

Similarly, the maximum ratio of total debt service to income acceptable to FHA is 41 percent, which is generally high relative to prime standards, but well below what passes in the nonprime sector.

A borrower who meets FHA credit standards will usually do better with an FHA loan than with a subprime loan, despite having to pay a mortgage insurance premium. The rate will be lower, the borrower will have access to a large menu of mortgages, and there are no prepayment penalties. Most mortgages in the subprime market are 2-year adjustables with large margins, which means a high probability of a rate increase after two years, and they have prepayment penalties, usually for three years.

Loan Limits: The loan limits on FHAs are a major deterrent. HUD has asked Congress to allow the same loan amounts on FHAs as on loans purchased by Freddie Mac and Fannie Mae. In 2006, this would have meant an increase to $417,000 uniform across the country.

Down Payment Requirements: In 2000, FHA's 3 percent down payment compared with 5 percent on most conventional loan programs. In 2006, however, zero-down loans were widely available in the conventional sector, while the FHA minimum of 3 percent remained unchanged. Since zero-down loans have long been available under the VA program, FHA is now the only sector that does not have them.

This disadvantage of FHA is partially offset by down-payment-assistance programs available to FHA borrowers. One form of such assistance is second mortgages at preferential rates, which is the preferred method of public agencies at the city, county or state levels. These agencies have their own eligibility rules independent of FHA.

A second form of assistance is cash contributions from nonprofit corporations. These have no repayment obligation, but the funds provided come from home sellers who take account of the contribution in setting their sales prices.

Neither type of assistance is a good substitute for a zero-down program, a bill for which was introduced in Congress in 2004. So far, however, it has not been passed.

Interest-Only Mortgages and Option ARMs. These instruments exploded in popularity after 2000, but were not available under FHA and there is little likelihood that they ever will.

Prospects For a Revival in FHA's Market Share. Congressional authorization of no-down-payment loans and a rise in loan limits would increase FHA's market share. So would an increase in public awareness that some subprime borrowers would qualify for, and do better with FHA loans.

A marked increase in FHA's market share would result from an explosion in foreclosures, which would cause a drastic restriction of lending terms in the conventional sector. This is not something I would care to see, but if it happened we will be pleased that FHA was there to help cushion the blow.

The writer is professor of finance emeritus at the Wharton School of the University of Pennsylvania. Comments and questions can be left at www.mtgprofessor.com.

_________________________________________________________________________

What's Hot and What's Not in Home Design

Mark Nash, the Chicago-based real estate broker who penned 1,001 Tips for Buying and Selling a Home (Thomson/South-Western, 2004), has released a list of home features that remain popular among buyers and those that are no longer in vogue. His list is based on responses from more than 900 real estate professionals nationwide.

For example, practitioners surveyed reported that the inability to keep stainless steel appliances, glass-front cabinets, and vessel-style sinks clean has caused them to fall out of favor with buyers. Also, spiral staircases have become less popular, particularly among buyers with young children.

As for what's "in," Nash found buyers are increasingly looking for some of the following features in homes:

Glass bathroom and kitchen tiles.

His-and-her home offices complete with fiber-optic cables for Internet connectivity.

Wood floors — except for those made of bamboo, which is not as durable.

Extra storage space in the form of linen closets, pantries, and luggage rooms.

With a large supply of unsold homes on the market, practitioners note that buyers have become pickier and expect homes to be in move-in condition.

Source: Washington Post, Kirstin Downey (01/06/07)

© Copyright 2006 Information Inc.

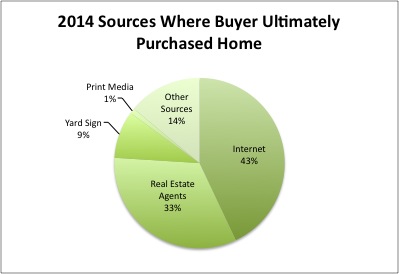

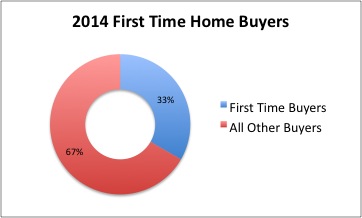

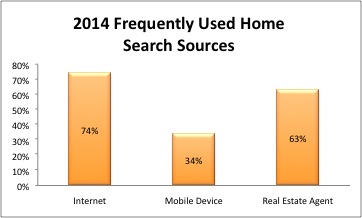

The most useful information for sellers and their agents is to be found in the section on the home search process. While the survey results are not significantly different from those of recent years, the trends continue. For example, this year 74 percent of buyers said that they used the internet frequently during the search process. In 2003 that number was only 42%. This past year 34% of buyers said that they frequently used a mobile or tablet application. That is a newer and growing phenomenon. 63% of buyers said that they frequently relied on a real estate agent for information.

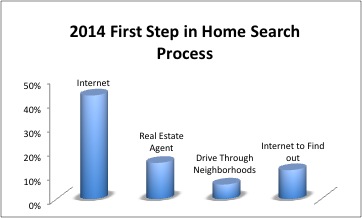

The most useful information for sellers and their agents is to be found in the section on the home search process. While the survey results are not significantly different from those of recent years, the trends continue. For example, this year 74 percent of buyers said that they used the internet frequently during the search process. In 2003 that number was only 42%. This past year 34% of buyers said that they frequently used a mobile or tablet application. That is a newer and growing phenomenon. 63% of buyers said that they frequently relied on a real estate agent for information. Forty-three percent of buyers went to the internet as the first step in the home search process. 15% contacted a real estate agent first, and 6% began by driving through neighborhoods looking for homes for sale. 12% first went online to find out about the process.

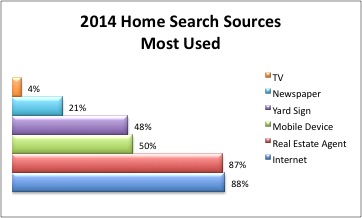

Forty-three percent of buyers went to the internet as the first step in the home search process. 15% contacted a real estate agent first, and 6% began by driving through neighborhoods looking for homes for sale. 12% first went online to find out about the process. Buyers use multiple sources of information in the process of looking for a home. Far and away the most used sources are on-line websites (88%) and real estate agents (87%). Mobile or tablet applications (50%) have replaced yard signs as the third most used source of information. Still though, 48% of buyers indicate that yard signs are one of their sources of information. Only 21% of buyers indicate that they used newspaper ads as an information source. A mere 4% garnered information from television.

Buyers use multiple sources of information in the process of looking for a home. Far and away the most used sources are on-line websites (88%) and real estate agents (87%). Mobile or tablet applications (50%) have replaced yard signs as the third most used source of information. Still though, 48% of buyers indicate that yard signs are one of their sources of information. Only 21% of buyers indicate that they used newspaper ads as an information source. A mere 4% garnered information from television.